If you’re a homeowner in need of financing, you may have heard of HELOCs. But what exactly are they, and how can they benefit you?

Table of Contents

What is HELOCs

HELOCs, or Home Equity Lines of Credit, are a type of revolving credit that uses the equity in a borrower’s home as collateral. Essentially, a HELOC allows a homeowner to borrow money against the equity they have built up in their home. The amount that can be borrowed is determined by the value of the home and the amount of equity the borrower has in it.

HELOCs have a draw period during which the borrower can access the funds as needed, and a repayment period during which the borrower must repay the borrowed amount plus any interest and fees.

How does a HELOC work?

HELOC works like a revolving line of credit, allowing you to borrow and repay funds as needed over a set period of time. HELOCs typically have lower interest rates than credit cards or personal loans, making them a popular option for financing home improvements, debt consolidation, and other expenses. To qualify for a HELOC, you will need to have a good credit score, a stable income, and sufficient equity in your home.

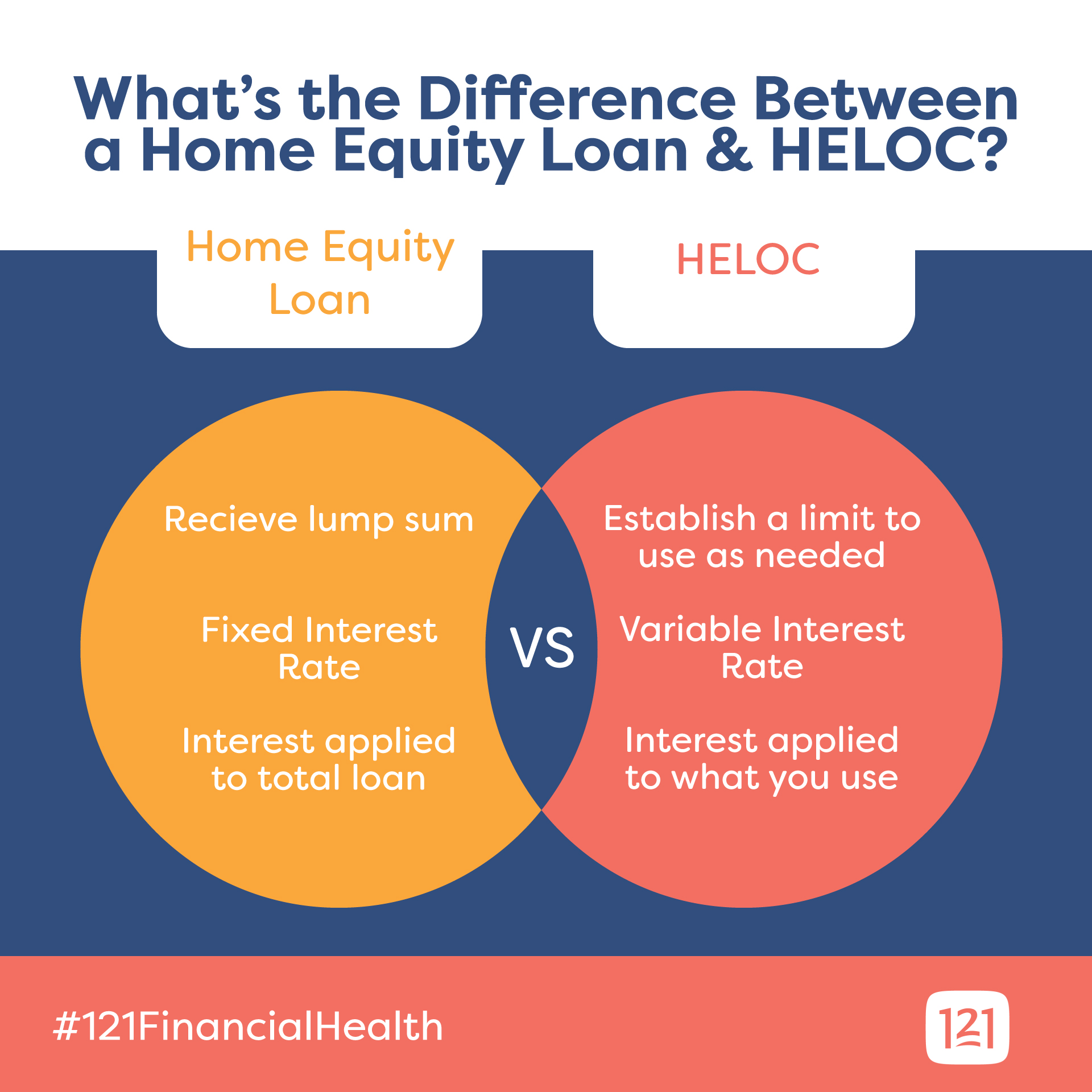

What is the difference between a HELOC and a home equity loan?

Homeowners have a variety of options when it comes to borrowing money against the equity in their homes. Two of the most popular options are home equity loans and home equity lines of credit (HELOCs). While both of these financial products allow you to borrow money using your home as collateral, there are some key differences between the two.

A home equity loan is a lump-sum loan that is secured by your home. You receive the entire loan amount upfront and then make fixed monthly payments over a set period of time. The interest rate for a home equity loan is typically fixed, which means it won’t change over the life of the loan.

A HELOCs, on the other hand, is a revolving line of credit that you can draw from as needed. You are given a credit limit, and you can borrow up to that amount over the life of the loan. As you repay the money you borrow, you can draw on the credit line again. HELOCs typically have variable interest rates, which means the rate can fluctuate over time.

One key advantage of a HELOC is that you only pay interest on the amount you borrow. With a home equity loan, you pay interest on the entire loan amount, even if you don’t use all of the money at once. This can make a HELOC a more flexible and cost-effective option for homeowners who need to borrow money for ongoing expenses, such as home improvements or college tuition.

How much can I borrow with a HELOC?

Basically, the amount you can borrow with a HELOC depends on several factors, including the amount of equity you have in your home, your credit score, and the lender’s policies.

Typically, lenders will allow you to borrow up to 85% of the equity you have in your home. To calculate the amount of equity you have, subtract the amount you owe on your mortgage from the current market value of your home. For example, if your home is worth $300,000 and you owe $200,000 on your mortgage, you have $100,000 in equity. 85% of $100,000 is $85,000, so that would be the maximum amount you could borrow with a HELOC.

However, just because you are eligible to borrow up to 85% of your equity doesn’t mean you should. It’s important to borrow only what you need and can afford to repay. It’s also important to consider the interest rates and fees associated with the HELOC, as these can add up over time and increase the amount you owe.

In addition, keep in mind that the amount you can borrow with a HELOC is not fixed. As you make payments on the line of credit, you may be able to borrow more. However, it’s important to always keep your debt-to-income ratio in mind and avoid borrowing more than you can afford to repay.

What are the interest rates for HELOCs?

Interest rates for HELOCs can vary depending on the lender, your credit score, the amount of equity in your home, and other factors. Generally, HELOCs have variable interest rates, which means that the rate can change over time based on the market conditions.

HELOC interest rates are typically based on the prime rate, which is the interest rate that banks charge their best customers. The prime rate is influenced by the federal funds rate, which is set by the Federal Reserve. When the federal funds rate goes up, the prime rate and HELOC interest rates are likely to go up as well.

In conjunction with the interest rate, there may be other fees associated with a HELOC, such as application fees, annual fees, and closing costs. Some lenders may also offer promotional rates or waive certain fees to attract customers.

How long is the repayment period for a HELOC?

The repayment period for a Home Equity Line of Credit (HELOC) is typically 10 to 20 years, with a draw period of 5 to 10 years. During the draw period, you can borrow money from the line of credit, up to your credit limit, and you only have to make payments on the interest. However, after the draw period ends, you enter the repayment period, and you must start making payments on both the interest and the principal.

During the repayment period, your payments will be higher because you have to pay off the principal in addition to the interest. The amount of your payment will depend on your interest rate, the remaining balance on your HELOC, and the length of the repayment period. You can choose to pay off your HELOC early or make additional payments, which can reduce your interest charges and shorten the repayment period.

Keep in mind that HELOCs have variable interest rates, which means that the interest rate can fluctuate over time. This can make it difficult to predict how much your payments will be during the repayment period. To avoid any surprises, it’s important to budget for higher payments during the repayment period and to be prepared for potential interest rate hikes.

What are the fees associated with a HELOC?

When considering a HELOC, it’s important to understand the fees that may be associated with the product. While every lender is different, here are some common fees that you may encounter:

- Application fee: This fee covers the cost of processing your application and can range from a few hundred dollars to over a thousand dollars.

- Origination fee: This fee is charged by the lender for setting up the HELOC and is typically a percentage of the credit limit, ranging from 0.5% to 1% of the total amount borrowed.

- Annual fee: Some lenders charge an annual fee just for having the HELOC, which can range from $50 to $100 or more.

- Closing costs: If you have to close out your HELOC, you may be charged closing costs, just like you would with a traditional mortgage. These can include appraisal fees, title fees, and attorney fees.

- Early termination fee: Some lenders may charge a fee if you pay off your HELOC early, typically within the first few years of the loan.

- Maintenance fee: Some lenders charge a monthly maintenance fee for the life of the loan, which can range from $10 to $50 or more.

Most importantly, ask your lender about any potential fees before you sign up for a HELOC, so you can weigh the costs and benefits and make an informed decision about whether it’s the right financial product for you. Keep in mind that some lenders may be willing to negotiate or waive certain fees, so it’s always worth asking if there’s any wiggle room.

What are the risks of using a HELOC?

While HELOCs can be a convenient and flexible way to borrow money, they do come with some risks that you should be aware of. Here are a few potential downsides to consider:

- Your home is on the line: With a HELOC, you’re borrowing against the equity in your home. If you’re unable to make your payments, the lender can foreclose on your home and take possession of it. This can be a significant risk, especially if you’ve borrowed a large amount or if the value of your home declines.

- Variable interest rates: Most HELOCs have variable interest rates, which means that your payments can change over time. If interest rates rise, your payments could become much higher, making it harder to keep up with your debt.

- Fees: HELOCs can come with a range of fees, including application fees, annual fees, closing costs, and more. These fees can add up quickly and make your borrowing more expensive than you anticipated.

- Temptation to overspend: Because HELOCs are flexible and easy to use, it can be tempting to borrow more than you need or to use the money for frivolous purchases. This can lead to a cycle of debt that’s hard to escape.

- Impact on your credit score: Like any type of borrowing, a HELOC can impact your credit score. If you miss payments or carry a high balance, your credit score could suffer.

Are there any tax benefits to using a HELOC?

When considering a HELOC (Home Equity Line of Credit), many people wonder if there are any tax benefits to using this type of loan. The answer is, it depends.

In general, the interest paid on a HELOC may be tax-deductible if the funds are used to improve your home. This is because the interest is considered to be a “qualified residence interest” under the tax code. However, there are some restrictions and limitations to be aware of.

First, the total amount of mortgage debt (including any HELOCs) that can be deducted is limited to $750,000 for mortgages taken out after December 15, 2017. For mortgages taken out before this date, the limit is $1 million. This means that if your mortgage debt exceeds these limits, you may not be able to deduct all of the interest on your HELOC.

Second, the funds from your HELOC must be used to improve your home in order for the interest to be tax-deductible. This means that if you use the funds for other purposes, such as to pay off credit card debt or take a vacation, the interest may not be deductible.

Note that to keep accurate records of how you use the funds from your HELOC in case you need to prove that the interest is tax-deductible. You should also consult with a tax professional to determine how a HELOC may impact your specific tax situation.

How do I repay my HELOC?

The question, “How do I repay my HELOC?” is an important one for anyone considering this type of financing. Repaying your HELOC properly can help you maintain good credit and avoid costly penalties. Here are some things to keep in mind when it comes to paying back your HELOC:

- Understand your payment schedule: Most HELOCs have a draw period and a repayment period. During the draw period, you can borrow against your line of credit and make interest-only payments. Once the draw period ends, you enter the repayment period, during which you’ll need to make payments on both principal and interest. Make sure you understand your payment schedule so you can plan accordingly.

- Set up automatic payments: Setting up automatic payments is a great way to ensure you never miss a payment. You can usually set up automatic payments through your lender’s website or by calling their customer service department.

- Make additional payments: Making additional payments on your HELOC can help you pay it off faster and save money on interest charges. If you receive a windfall or have extra money at the end of the month, consider putting it towards your HELOC.

- Avoid minimum payments: While it may be tempting to make minimum payments on your HELOC, doing so will only prolong your repayment period and cost you more in interest charges. Try to pay as much as you can each month to pay off your HELOC faster.

- Keep your credit score in mind: Late or missed payments on your HELOC can negatively impact your credit score. Make sure to pay on time and in full to maintain good credit.